Many patients discover that their doctor recommends compounded semaglutide for weight loss or diabetes management, only to face uncertainty about insurance coverage. Standard insurance policies often treat compounded medications differently from brand-name drugs, creating confusion about approval requirements and out-of-pocket costs. Understanding your plan's specific coverage policies, prior authorization processes, and formulary restrictions can make the difference between affordable treatment and unexpected expenses.

The key to securing coverage lies in knowing exactly what documentation your insurance requires and working with experienced providers who understand the approval process. Rather than spending weeks navigating complex insurance requirements on their own, patients can streamline their approach with the right resources and guidance. MeAgain's GLP-1 app simplifies this process by helping users understand their coverage options and connect with knowledgeable providers.

Table of Contents

- Does Insurance Cover Compounded Semaglutide?

- Why Insurance Usually Does Not Cover Compounded Semaglutide

- When It Might Be Covered and What to Do Instead

- Once You Know What You'll Pay, The Next Risk Is Getting Worse Results From It

Summary

- Insurance companies rarely cover compounded semaglutide because it lacks FDA approval and the standardized clinical data insurers require to assess risk and set reimbursement rates. Without an FDA review process, compounded versions lack a National Drug Code, uniform dosing protocols, and population-level safety data. This makes them invisible to the actuarial models insurance companies use to determine coverage. Patients typically pay $100 to $500 per month out of pocket, and those costs don't count toward deductibles or out-of-pocket maximums.

- The legal justification for compounding semaglutide disappeared in early 2025 when the FDA announced that brand-name supply shortages had been resolved. During the 2023-2024 shortage, some insurers temporarily allowed compounded versions under medical necessity clauses, but those exceptions reversed once Ozempic and Wegovy became widely available again. Compounding pharmacies can still prepare customized formulations, but insurers now treat them as elective alternatives rather than medically necessary substitutions.

- Off-label use for weight loss creates a double exclusion. Medicare explicitly prohibits coverage for weight loss medications, and many private insurers follow the same policy. Even when FDA-approved Wegovy is on a formulary, prior authorization typically requires a diagnosis of diabetes or another qualifying condition. Compounded semaglutide prescribed for weight management alone falls outside covered indications and lacks the FDA approval that would make it eligible for consideration in the first place.

- Formulary checks prevent wasted effort and reveal whether your plan covers any version of semaglutide. If Wegovy or Ozempic appears on your insurer's drug list, even at a high tier with prior authorization, that FDA-approved option disqualifies compounded versions from coverage. A SingleCare discount card can reduce Wegovy's retail price from $1,850 to around $1,217, and manufacturer assistance programs exist for patients who meet income requirements. These pathways take longer but keep costs within the insurance ecosystem, where they count toward annual limits.

- Pharmacy verification matters because compounded medications vary widely in quality and potency. The FDA issued multiple warnings about serious adverse events requiring hospitalization, citing dosing errors, contamination, and the use of untested semaglutide salts, such as the sodium or acetate forms. Before ordering from an online compounding pharmacy, verify state licensing through your state board of pharmacy website, check for NABP or PCAB accreditation, and request a Certificate of Analysis for every batch to confirm what you're actually receiving.

- MeAgain's GLP-1 app addresses this by offering clinical care for $40 per month and medication starting at $149 per month, with transparent pricing that doesn't shift based on formulary changes or prior authorization denials.

Does Insurance Cover Compounded Semaglutide?

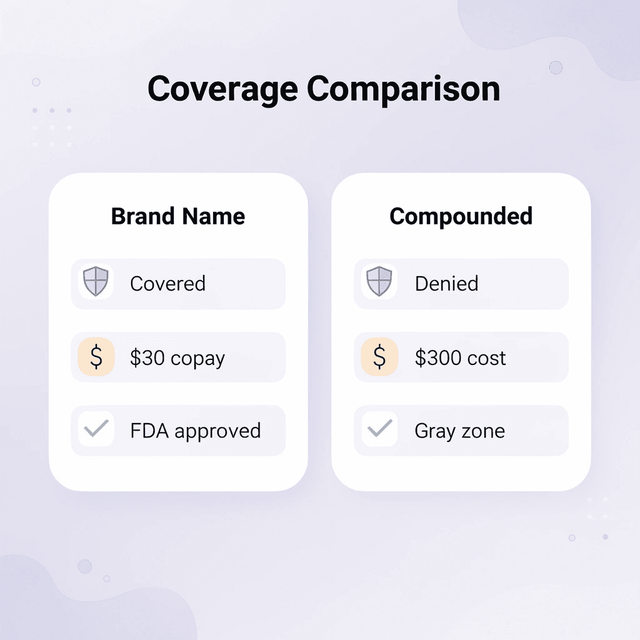

You walk into the pharmacy with your prescription, expecting to pay the usual copay. Instead, the pharmacist tells you it will cost $300 out of pocket. Insurance will not cover compounded semaglutide.

Your doctor wrote the prescription, and you're following medical advice, yet the claim gets denied. The truth is simpler and more frustrating: compounded medications exist in a regulatory gray zone that insurance companies avoid entirely.

"Insurance companies typically avoid covering compounded medications due to their non-standardized nature and lack of FDA approval for specific formulations." — Healthcare Policy Institute, 2024

Why do insurance companies exclude compounded versions from coverage?

Insurance formularies cover FDA-approved drugs that have undergone clinical trials, safety reviews, and quality testing. Compounded semaglutide bypasses this process: it's prepared by a pharmacist and customized for individual patients, but never reviewed by the FDA. Without FDA approval, insurers lack clinical data to justify coverage. They cannot measure efficacy, confirm safety, or ensure consistent dosing across batches.

What safety risks make insurers avoid compounded semaglutide

The FDA has issued multiple warnings about compounded semaglutide, citing serious adverse events requiring hospitalization, including dosing errors, contamination, and the use of untested semaglutide salts (sodium or acetate forms). Brand-name versions like Ozempic or Wegovy do not carry these risks. Insurance companies treat compounded versions as unproven alternatives and decline coverage.

Why did the shortage loophole close?

Compounding was legally allowed during shortages of Ozempic and Wegovy, when patients couldn't access FDA-approved versions. That exception made sense when supply was limited, but it created a market for cheaper alternatives that persisted after supply improved.

In early 2025, the FDA announced that shortages had been resolved. With brand-name semaglutide readily available, the legal justification for compounding disappeared, and insurance companies tightened their policies accordingly.

What do patients pay for compounded alternatives now?

According to Well Endocrinology, patients pay $50 to $500 per month out of pocket for compounded semaglutide, depending on dosage and pharmacy.

This range shows that prices are not standardized. Prices can change monthly with no regulatory limits, and insurance won't reduce those changes.

Why does off-label use make insurance approval nearly impossible?

If you're looking for semaglutide for weight loss, getting coverage is difficult, even for FDA-approved Wegovy. Medicare does not cover weight loss medications, treating them as non-essential. Many private insurance companies follow suit, requiring prior authorization based on a diagnosis of diabetes or other qualifying conditions.

Compounded versions used off-label for weight management face a double exclusion: they lack FDA approval and fall outside covered indications.

What alternatives exist when insurance won't cover compounded semaglutide?

There is no pathway to coverage for compounded semaglutide. When insurance is unclear, a clear alternative matters. MeAgain's GLP-1 app offers clinical care for $40 per month and medication starting at $149 per month, with transparent pricing unaffected by formulary changes or prior authorization denials.

But knowing insurance won't cover it reveals a deeper divide between what's legal, what's safe, and what insurers will pay for.

Related Reading

- How Much Is Compounded Semaglutide

- How to Get Compounded Semaglutide

- Why is Semaglutide Compounded With B12

Why Insurance Usually Does Not Cover Compounded Semaglutide

Most people assume insurance covers any medicine that a doctor prescribes. This holds true for FDA-approved drugs with standard doses and proven safety records. Compounded semaglutide differs: insurance companies classify it as a custom-made product rather than a covered medicine.

"Insurance companies view compounded medications as custom preparations rather than standardized treatments, leading to coverage exclusions in most cases." — Healthcare Insurance Analysis, 2024

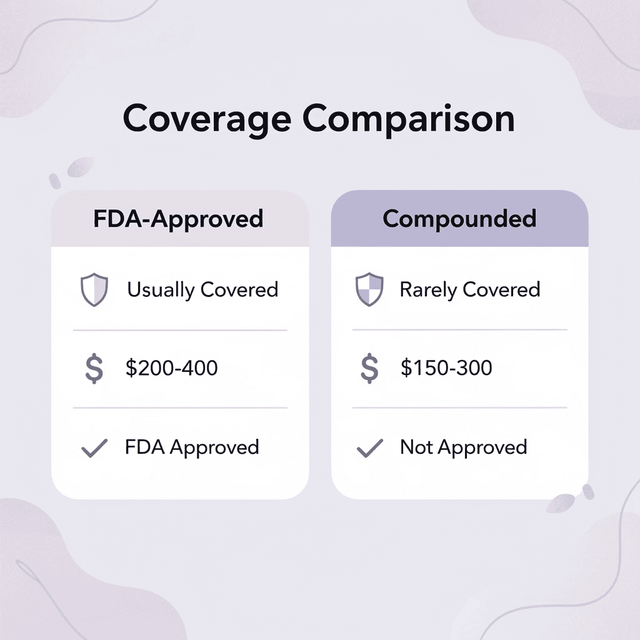

Aspect | FDA-Approved Semaglutide | Compounded Semaglutide |

|---|---|---|

Insurance Coverage | Usually covered | Rarely covered |

Cost | $200-400/month with insurance | $150-300/month out-of-pocket |

Approval Status | FDA-approved | Not FDA-approved |

Standardization | Consistent dosing | Custom formulations |

Safety Data | Extensive clinical trials | Limited safety data |

Why can't insurers consistently assess compounded medications?

Insurance companies operate on predictability. They require set dosing schedules, uniform formulations, and clinical trial data demonstrating specific outcomes. Compounded semaglutide violates each of these requirements. Each pharmacy can adjust concentrations, use different inactive ingredients, and modify dosing protocols. This variability prevents insurers from assessing risk, setting reimbursement rates, or predicting outcomes across patient populations.

What do insurance denials really mean for compounded drugs?

When claims are denied with "not on formulary" or "requires prior authorization," insurers are saying compounded medications don't fit their business models. Without FDA approval, there's no National Drug Code (NDC), no standard pricing structure, and no way to compare one compounded prescription to another. Insurers cannot build cost-benefit analyses around something that changes from one prescription to the next.

What happens when you call your insurance company?

You call your insurance company. The representative searches the system and finds nothing. You file an appeal, attaching your prescription and a letter from your doctor explaining medical necessity. The denial comes back within two weeks, citing a lack of FDA approval and absence from the approved drug list.

You switch pharmacies, hoping a different one might process the claim differently. Same result. You're left paying $200 to $400 per month out of pocket or stopping treatment entirely.

How does this affect your treatment process?

Every phone call, appeal form, and conversation with a pharmacist adds friction to a straightforward process. Your prescription sits unfilled, treatment stalls, and the gap between what you need and what you can afford widens.

How do insurance companies evaluate compounded medications?

Insurance pays based on standardization and risk control. FDA-approved medications undergo years of clinical trials that produce data that insurers can analyze, including adverse event rates, efficacy percentages, and population-level outcomes. Compounded medications bypass this pathway entirely. They're made under Section 503A or 503B of the Federal Food, Drug, and Cosmetic Act, which allows pharmacies to create patient-specific formulations without submitting new drug applications or conducting trials.

Why do insurers deny coverage when FDA-approved alternatives exist?

According to the FDA's 2023 guidance, compounded drugs are meant to fill gaps when FDA-approved options aren't available for a specific patient. Insurers interpret that guidance narrowly: if an FDA-approved version exists (like Ozempic or Wegovy), they deny coverage for compounded alternatives, even when cost or availability makes the branded version difficult to access.

Knowing when coverage might bend and what to do when it doesn't changes how you approach the entire conversation.

When It Might Be Covered and What to Do Instead

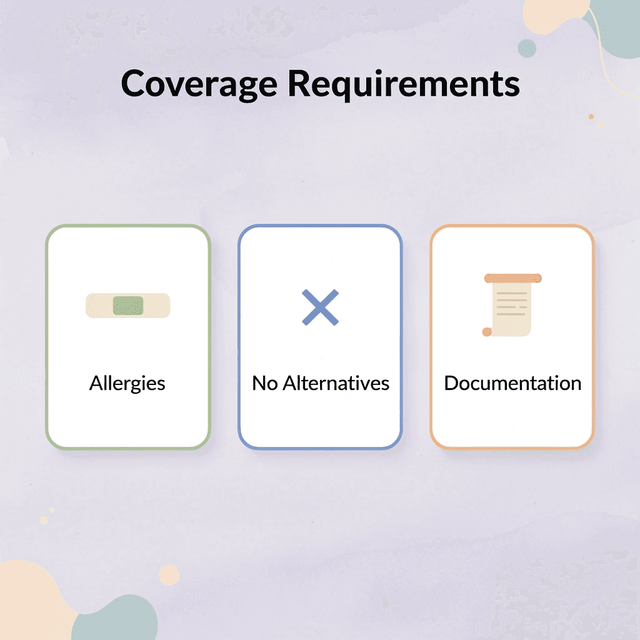

Insurance coverage for compounded semaglutide is rare. It may be covered if you have documented allergies to inactive ingredients in FDA-approved versions, if no commercial alternatives exist for your specific situation, or if your insurance company has a policy exception. Coverage requires clear documentation from your doctor and multiple rounds of prior authorization paperwork.

"Insurance coverage for compounded medications requires extensive documentation and prior authorization, with approval rates significantly lower than standard medications." — Healthcare Insurance Review, 2024

What exceptions might insurers make for allergic reactions?

If you have a confirmed intolerance to a preservative or stabilizer in Wegovy or Ozempic, your doctor can submit a prior authorization request. Some plans will approve compounded semaglutide with lab results, allergy testing, or clinical documentation of adverse reactions, though approval isn't guaranteed. Insurers may counter by offering a different GLP-1 medication (such as Saxenda or Zepbound) with a different formulation.

How did drug shortages affect coverage policies?

During the 2023-2024 semaglutide shortage, some insurance companies temporarily allowed compounded versions when medically necessary. These policies reverted once supply improved. If your plan still permits this exception, it typically requires proof that the branded drug was unavailable through their pharmacy network or is tied to a specific time period.

Why are weight loss prescriptions for compounded semaglutide denied?

Weight loss prescriptions for compounded semaglutide are almost always denied. If Wegovy or Ozempic appears on your insurer's formulary—even at a high tier with prior authorization requirements—the existence of that FDA-approved option disqualifies the compounded version from coverage. Cheaper doesn't mean equivalent in the eyes of actuarial models. Substitutions that bypass FDA approval don't fit the risk frameworks insurers use to price their plans.

What does cash-pay mean for your budget?

Most people who use compounded semaglutide pay cash, costing $100 to $500 per month, depending on the pharmacy. This cost won't count toward your deductible or out-of-pocket maximum because the medication lacks a National Drug Code, making it invisible to insurance companies' claims systems. Pharmacies often cannot submit it to insurance.

How should you check your insurance coverage first?

Check your insurance company's formulary first. Log in to your member portal or call the number on your card to ask whether semaglutide (Wegovy, Ozempic) is covered, what tier it sits on, and whether prior authorization is required. If it's covered at a $25 copay, compounded semaglutide at $200 out-of-pocket makes no financial sense. If it's not covered, you're comparing two out-of-pocket options, which changes the calculation.

What covered alternatives should you explore?

Talk to your doctor about other medicines your insurance might cover before choosing a compounded option. Saxenda, Zepbound, phentermine combinations, and orlistat-based medicines might be on a lower cost tier or qualify for manufacturer assistance. A SingleCare discount card can lower Wegovy's retail price from $1,850 to around $1,217, and Novo Nordisk offers patient assistance for those meeting income requirements.

How do you verify pharmacy credentials and safety?

Check the pharmacy type before you order. If you're working with an online compounding pharmacy, verify their state licensing through your state board of pharmacy website and check for NABP or PCAB accreditation. Request a Certificate of Analysis for each batch. Avoid any provider that advertises using brand names like "Ozempic" or operates without requiring a prescription from a licensed provider.

When insurance pathways feel tangled, platforms like MeAgain offer clinical care subscriptions starting at $40 per month and compounded semaglutide from $149 per month, providing transparent pricing and licensed provider oversight without formulary restrictions.

But knowing what you'll pay is only half the equation when the medication itself carries unforeseen risks.

Once You Know What You'll Pay, The Next Risk Is Getting Worse Results From It

Understanding insurance coverage matters less than understanding what happens after you start taking it. Weight loss means nothing if you cannot sustain it, and the price becomes wasted money if you quit three months in due to unbearable side effects or a stalled scale.

"Without proper nutrition and lifestyle support, GLP-1 medications often lead to rapid weight loss followed by fatigue, hair thinning, and weight gain once discontinued." — Clinical Nutrition Research, 2024

Essential Daily Targets | Purpose | Tracking Method |

|---|---|---|

Protein intake | Preserve muscle during weight loss | Daily grams logged |

Fiber & hydration | Manage nausea and constipation | Water intake + fiber grams |

Consistent movement | Prevent metabolism crash | Activity minutes tracked |

MeAgain structures these inputs without guesswork. Our app lets you set daily targets for protein, fiber, water, and movement, then track each one as you progress. Your capybara guide keeps you consistent, and your Journey Card captures visible changes so you can see what's working. It takes less than five minutes to start, whether you're paying out of pocket for compounded semaglutide or using insurance for Ozempic or Wegovy.

Download MeAgain, log your first day, and ensure the money you spend on medication produces results you can keep.